EU Tech Sovereignty: Made Real

Zero political theater. Turn on OT. Buy local startups.

Intro

After months writing about American reshoring — whose constraint is certainly not economic capacity — and what that shift opens up for Europe, Italy and Germany first among them, it is time to confront the harder subject: sovereignty.

A subject routinely mishandled, sometimes out of convenience, sometimes out of technical illiteracy. I have heard ministers and chief executives describe “European AI sovereignty” in ways indistinguishable from fairy tales. None of it is operational.

Europe is aware it failed to keep pace.

It let the United States do the investing, the building, the capital-risking, and positioned itself above the market instead — as regulator, guardian, standard-setter.

Some useful ideas came out of that role. But industrial systems are not built from above the market. They are built inside it.

Over the past weeks, here in Silicon Valley, I have spent time with people who built parts of that world directly — fog computing, hybrid cloud, parts of the quantum stack. From that, two concrete paths to sovereignty take shape. Not a European chatbot. Not another layer of political theater. The industrial infrastructure Europe still controls, and the local demand that can finance and densify it.

Part 1 — Sovereignty Starts from Infrastructure

WHERE SOVEREIGNTY ACTUALLY RESIDES

Technological sovereignty is a question of infrastructure. Everything else is stagecraft.

This needs saying immediately, because public debate is still confused about where sovereignty actually resides. An open-source AI model, an interface in Italian — or German, or French — a model trained on European values, a startup headquartered in Paris: none of this is sovereignty.

These things sit at the top of the stack.

They are the visible layer, and usually the layer that matters least.

Sovereignty means controlling the operational layers underneath the interface:

Compute, cloud, networking — where everything runs and everything travels.

Semiconductors and rare earths — China refines over ninety percent of them, and the bottleneck is whoever processes the rock, not the rock itself.

Energy and deployment capacity — the difference between a system that is designed and a system that actually runs under pressure.

These are the layers nobody sees. Which is precisely why they disappear so easily when strategies get written.

Today Europe controls almost none of them. GPUs are American. Hyperscalers are American. Advanced semiconductors move through a supply chain distributed across the United States, Taiwan, Korea and the Netherlands, while the strategic center of gravity remains outside Europe. HBM memory, EDA tooling and most AI deployment infrastructure follow the same pattern.

Running “European AI” on top of this stack changes the label, not the dependency.

This is not a judgment.

It is simply the starting condition of any politically and strategically serious conversation.

THE CLOCK RUNS FASTER THAN IT LOOKS

There is a clock attached to that reality, but it does not run on a fixed date.

The dynamic is not linear.

Infrastructure advantage compounds: every year European compute autonomy is postponed, the scale gap created by American and Chinese investment does not simply widen — it multiplies.

This is not ideology. It is arithmetic.

There is no precise deadline after which the race is lost; there is a process that makes recovery harder every quarter no one moves. Compound capital at that scale cannot be caught up through a single industrial cycle.

Building infrastructure requires decades, capital, energy, industrial coordination and supply-chain density. The United States accumulated this position through twenty years of continuous investment. It did not declare it into existence.

Believing Europe can reproduce the same outcome through announcements and sovereign funds is an expensive illusion because it redirects resources toward objectives that cannot realistically be achieved within the available timeframe.

The problem, therefore, is not “building a European ChatGPT.” That framing misses the point from the beginning.

The issue is infrastructure. And in a world where almost no company functions without Microsoft Word, treating the United States as a geopolitical enemy is childish and operationally unrealistic. The United States are part of the infrastructural reality within which Europe operates, and they will remain so for a long time.

Part of the European debate prefers resentment over analysis. It reacts emotionally to dependency instead of asking how that dependency was created in the first place. Dependency was not imposed. It emerged from twenty years of investments Europe chose not to make. First close the gap. Then, maybe, argue about who is to blame.

The asymmetry exists. The only serious question is how to turn it into leverage.

Part 2 — To Understand Cloud, Think About Cars

Europe lost the hyperscaler race for the same reason it struggled with electric vehicles: late entry into vertically integrated systems already dominated by others. The comparison matters because it explains a mechanism, not just an outcome.

Take batteries. China did not win because labor was cheaper — that explanation is convenient, and mostly wrong.

China won because it integrated the entire chain: extraction, refining, cell chemistry, manufacturing, software, deployment and charging infrastructure.

Every layer reinforced the others. In systems like this, advantage is not additive. It compounds. Improvements in one layer reduce costs and increase efficiency across all the others.

Cloud evolved in much the same way. American hyperscalers do not simply sell computing. They sell an integrated stack: data centers, networking, in-house silicon, developer tooling, orchestration software and now AI infrastructure itself. Whoever enters this market today is not competing against a product. They are competing against twenty years of integration.

During the same period, Europe remained fragmented. Twenty-seven markets, twenty-seven procedures, national protectionisms disguised in bureaucratic language. And while the United States and China were building vertically integrated digital infrastructure, Europe comfortably accepted not investing in digital infrastructure — exactly as it did with defense.

The issue is not competence. Europe still has extraordinary engineers, strong research and some of the best manufacturing capability in the world.

The issue is method.

And culture.

For fifteen years Europe treated digital infrastructure as an expense rather than a strategic asset. At the same time, regulation increasingly preceded industrial density. In California, engineers build and regulators follow.

In Europe, the market itself — business and consumer alike — is reluctant to buy from startups. Weak traction leaves them underfunded, and for the most critical innovators the only way out is often public money — funding from state vehicles.

So AI companies grow slowly. And the more they depend on state funds, the more the regulator's grip tightens: the same hand that keeps them alive also holds them back. Regulation matures before a critical mass of companies even exists — so the rules land on startups too fragile to absorb them, forcing them to spend on compliance what they should be spending on the product itself.

THE IMPOSSIBLE TRIAD — AND ITS BLIND SPOT

American analysts — particularly around the Atlantic Council ecosystem — have turned this criticism into a structured argument. Europe, they claim, wants three mutually incompatible things at once: maximum sovereignty, minimum cost and frontier-level performance. The impossible triad. According to this view, sovereign silos inevitably become slower, more expensive and technologically inferior.

Working from Palo Alto, I hear this argument often. It should be taken seriously rather than dismissed as bad faith.

It is valid — under one condition. If the goal is full-stack sovereignty, rebuilding everything from silicon to chatbot, then yes: the triad becomes impossible and pursuing it becomes a waste of resources.

But the argument also has a blind spot.

The triad only becomes impossible if sovereignty is pursued everywhere. It becomes manageable the moment Europe stops competing where the race is already lost and focuses instead on the layer where it still retains structural density.

The physical world.

The asymmetry around cloud infrastructure is real, and it will not disappear. But asymmetries, in industry, eventually become trade. OT is not glamorous, and venture capital — heavily concentrated in Silicon Valley — has historically preferred consumer software over industrial systems.

Which leaves one of the most strategically important domains relatively open.

Europe still controls that industrial layer.

And it is not marginal.

Part 3 — OT is Europe’s Real Leverage

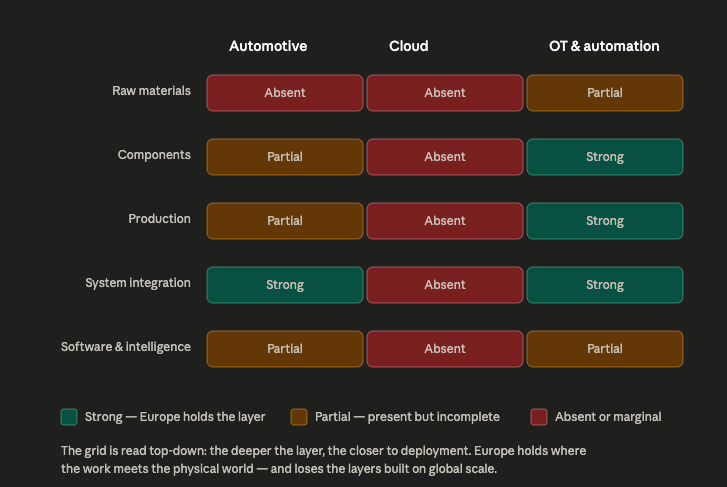

When it comes to consumer AI infrastructure, Europe is behind. There is no reason to soften that reality.

At another layer, however, the position reverses completely: manufacturing, industrial automation, OT, robotics and cyber-physical integration.

Here Europe still has density, installed base and decades of operational knowledge that cannot be replicated through a funding round.This is where technological sovereignty can become real instead of remaining a slogan.

The next layer of value sits in the physical world, and in AI applied to that world. Europe now faces a very simple choice. It can wait — exactly as it did with cloud — while American companies build the systems and Europe’s best engineers relocate to Silicon Valley to work on them.

…

Or it can build on what it already possesses: industrial environments, field-level systems, edge data lakes, inference running near the machine itself, operational protocols and enormous amounts of industrial data generated by systems already in production.

The factory floor is the one place Europe never stopped being sovereign.

The edge matters for technical reasons.

Latency, service continuity and data control all require inference to run near the machine. Factory-field systems. Infrastructure capable of reasoning locally.

This layer lives inside industrial environments rather than hyperscaler data centers, and the industrial environments are already here.

One factor remains consistently underestimated: energy.

Industrial intelligence runs where reliable, affordable power exists — and Europe's manufacturing core, Germany and Italy above all, does not yet have it on those terms. Italy is a clear case: as of 2025 it still imports roughly 15% of its electricity outright, and close to half of what it does generate at home runs on imported gas — which is why its power is both exposed and expensive.

There is no point claiming technological sovereignty while the energy underneath it is, to this degree, someone else's.

Reliable power is infrastructure exactly as much as silicon is — and it is the precondition the rest of this argument quietly rests on.

SOVEREIGNTY YOU CAN CARRY IN YOUR POCKET

Does OT matter more than GPT? There are two answers.

One is timing. For Europe, it is too late to pour unlimited amounts of capital into chasing systems that already escaped years ago.

The second is structural. OT is the nervous system supporting logistics, energy, critical infrastructure and defense. Disable that nervous system and the country stops functioning.

This matters because modern defense increasingly depends on compute, edge systems, manufacturing and resilient operational infrastructure. A country that gives away these layers gives away part of its defensive capability, regardless of how many strategic documents it publishes.

The next time someone talks about sovereignty — on stage or at a conference — look at the object in their hand. A phone designed in the United States, assembled across Taiwan and China, running on Chinese memory, a Korean battery and American software. And almost none of the managers or politicians discussing sovereignty would survive a week without Office. Talking about sovereignty while lacking proprietary density in low-level industrial systems is a contradiction people literally carry in their pockets.

There is also something rarely said openly because it risks sounding protectionist. Prioritizing domestically produced industrial and defense systems is standard doctrine for every country with a serious defense apparatus, including the United States. Some layers supporting operational continuity need to remain inside supply chains where some degree of control still exists.

THE TRANSATLANTIC OPENING

There is also a historic opportunity emerging right now. The United States have started a reshoring cycle of historic scale, and reindustrialization requires precisely the layers where Europe remains strong: automation, cyber-physical integration, precision manufacturing and control systems.

I have written about this elsewhere as a transatlantic opportunity; here I am looking at the European side of the same game. Selling into that market does not weaken European sovereignty. It demonstrates that Europe’s OT density still has real market value, and that value can finance its next stage of growth.

You trade as equals when you possess something the other side genuinely needs.

OT therefore becomes the layer where the asymmetry described flips. Europe is not creating an advantage from scratch. It is activating one it already possesses and has largely left dormant.

Which leaves the most practical question of all.

Who builds this ecosystem?

And who feeds it?

Part 4 — Buy Local Startups First

DEMAND IS THE STEERING WHEEL

The same principle applies on both sides of the Atlantic. The fastest form of technological sovereignty is not a hundred-billion-euro sovereign fund. It is local demand.

Technology sovereignty made easy?

Buy from local startups first.

This works in Milan exactly as it works in Palo Alto.

It is not a European rule. It is an industrial rule.

Technological ecosystems are not born from patents or laboratories.

They emerge from customers.

Without local procurement, the sequence is always the same: startups relocate where the market exists, talent follows them, deployment happens elsewhere and capital concentrates around deployment.

For Europe, the principle has a second effect.

Buying local products and financing local startups accelerates the construction of the OT stack itself while shaping the direction of growth. Whoever buys determines which companies survive, which sectors densify and where expertise accumulates.

Demand is the steering wheel.

If European governments and large corporations continue buying only foreign stacks, Europe remains what it already is: a consumption market.

A place where technology gets used rather than built.

This is industrial policy, not nationalism. The criterion is not the supplier’s flag.

The criterion is whether a local market exists at all, because ecosystems without nearby customers do not improve. They disappear. Or relocate.

WHY STARTUPS, NOT INCUMBENTS

Europe’s problem is not competence. It is mindset.

Asking a manufacturing group (incumbents) that spent fifty years building advantage through mechanical precision to suddenly become software-driven means asking it to “reject” its own culture, incentives and command structure. The mindset that is actually needed — software driving the atoms — is something I have tried to describe elsewhere: it is not decreed, it is grafted in.

Transformation-from-within is mostly conference mythology.

In practice, industrial transitions usually emerge OUTSIDE incumbents.Anduril and Palantir were not born inside legacy defense contractors reformed from within. They emerged -as startups- outside the system, software-first, and forced incumbents to react. They reimagined defense through software rather than steel because they did not have decades of operational inertia to defend.

Buying local startups therefore matters because it injects a different operational logic into the system itself instead of waiting for the old one to convert spontaneously.

It creates pathways for younger engineers who currently see no future locally and leave. And it allows Europe to rethink strategic sectors — defense first — through organizations built around software-defined systems rather than mechanical-era structures.

This is already visible in the market.

Mistral and Aleph Alpha win in heavily regulated environments because American models are primarily accessed through APIs running on proprietary cloud infrastructure, while European players increasingly license models that run directly on the customer’s own servers.

It is easy to dismiss this as a compliance workaround. But reducing it to compliance mistakes the visible tip for the iceberg underneath. Self-hosting does not win because of regulation alone. It wins because three independent forces push in the same direction:

Compute keeps getting cheaper. Workloads that required data-center scale ten years ago increasingly fit inside a rack next to the machine itself. Inference close to the data stops being a compromise and becomes the natural architecture.

The nature of sensitive data changes. Once robots enter homes, factories and critical infrastructure, the sensitive layer is no longer abstract metadata. It becomes spatial maps, industrial telemetry, operational behavior and the physical environments people inhabit.

Cloud-only is becoming unsustainable. At planetary scale, the economics no longer hold. Even AWS increasingly pushes hybrid and edge infrastructure. The market already understands this shift, even if much of the public narrative still lags behind.

The future of AI applied to the physical world is distributed, local and physically close to the machine because the economics of the shift make reversal difficult. That future increasingly resembles OT itself.

And this is precisely where software-first startups gain structural advantage while cloud-only incumbents inherit structural constraints.

In sectors where this matters most — defense, industrial systems and strategic infrastructure — local procurement stops being a commercial choice.

It becomes three things at once:

capability retention — the skills and the supply chain stay where they can be reached;

operational sovereignty — the system keeps running when a decision taken elsewhere would otherwise stop it;

industrial continuity — the line between design and production does not break.

None of this can be rebuilt afterward, once it suddenly becomes urgent. It has to be built in advance — by buying, now, from those already building it.

Conclusion

Sovereignty cannot survive as a political slogan.

The debate changes the moment sovereignty is treated as operational capability rather than narrative — as infrastructure rather than ideology. Europe does not need to declare it into existence. It needs to activate the leverage it already holds, and build the market conditions that let that leverage compound instead of slowly dissolving.

Which leaves one decision, and it belongs to very specific people. The CEO signing the procurement contract. The minister approving the industrial budget. The defense organization deciding which systems enter the supply chain.

For forty years the industry ran on one principle: nobody ever got fired for buying IBM. The safest move was always the largest external vendor. If dependency emerged later, it stayed somebody else’s problem. That logic no longer holds. Buying dependency is no longer the cautious option — it simply externalizes the risk until the system itself becomes the bottleneck.

The question is no longer whether Europe can afford to build its own industrial and technological stack. It is whether it can afford not to.

Europe already controls part of the physical world where this matters. The window to act on it is open now, while American reshoring still runs ahead of the engineers and the automation capacity it needs. That window does not stay open. Either Europe moves while it can — and trades into a global market as an equal — or the United States close the gap themselves, and Europe is left with its domestic market alone. A basin of water. Not a blue ocean.

None of this works against the United States, or without them. It works only if Europe builds its own ground to stand on first. Sovereignty is not declared. It is made.

This article closes an arc of four earlier pieces on the physical world as the next layer of value: The New Industrial Mind on the return of hardware, Inside the Belly of the Physical AI Beast on industrial mindset, Physical AI vs Software AI on the economics of distributed intelligence, and California Sets the Pace of U.S. Reshoring on geography and infrastructure. This piece is the European reading of the same transition.

Be prepared for a long reading. But worth it.